Does My Renters Insurance Cover My Engagement Ring If It Goes Missing? The Big Question

Many people assume their renters insurance policy acts like a magic blanket, covering everything they own, no questions asked. You’ve got your policy, right? So if that beautiful engagement ring — or maybe that inherited watch from your grandma — vanishes, you’re all set. The short answer is yes, sometimes. The real answer is much more complicated.

See, standard renters insurance policies *do* cover personal property. That’s a fact. If a fire rips through your apartment in, say, Santa Monica or a thief breaks in while you’re vacationing in Palm Springs, your policy’s got your back for losses due to those specific events. But here’s where it gets interesting. Every policy has limits. Not just overall limits on your stuff, but specific “sub-limits” on certain types of property. Jewelry is almost always one of them.

And then there’s the “peril” part. Renters insurance typically covers “named perils” — a list of bad things like fire, theft, vandalism. What about “mysterious disappearance”? That’s when your ring is just… gone. You didn’t lose it to a fire. It wasn’t stolen from your home. It simply isn’t where you left it. Most basic renters policies won’t cover that. It’s a tough pill to swallow, especially when we’re talking about something so sentimental and valuable.

Okay, So What Are These “Limits” Everyone Talks About?

Let’s get down to brass tacks. Your average renters insurance policy in California will have a sub-limit for jewelry. This usually hovers somewhere between $1,000 and $2,500. Not per item, mind you. That’s the *total* amount the policy will pay out for *all* jewelry lost in a single incident, regardless of how many pieces you own or how valuable they are.

Imagine you live in the Valley, maybe near Encino. You’ve got a $10,000 engagement ring and a $5,000 diamond necklace. A burglar cleans out your jewelry box. Your policy has a $2,000 jewelry sub-limit. Guess what? You’re looking at a $13,000 loss out of your own pocket. That’s a huge difference. For most people, a $2,000 payout just won’t cut it when it comes to replacing cherished, high-value pieces.

What If I Have Several Pieces of Jewelry?

This is a common misconception. People think, “Oh, I have a few rings, a bracelet, a watch. If one goes, I’m covered up to the limit.” Not exactly. That sub-limit applies *per occurrence*. So if your entire jewelry collection, worth $20,000, is stolen, and your policy has a $2,500 jewelry sub-limit, you’re still only getting $2,500. It doesn’t matter if it was one item or twenty. The policy doesn’t care about the number of pieces; it cares about the *total value* of jewelry involved in that one incident. This is often a harsh reality check for renters.

How Can I Really Protect My Valuable Jewelry in California? Beyond the Basics

So, if standard renters insurance isn’t enough, what’s a savvy Californian to do? You’ve got options.

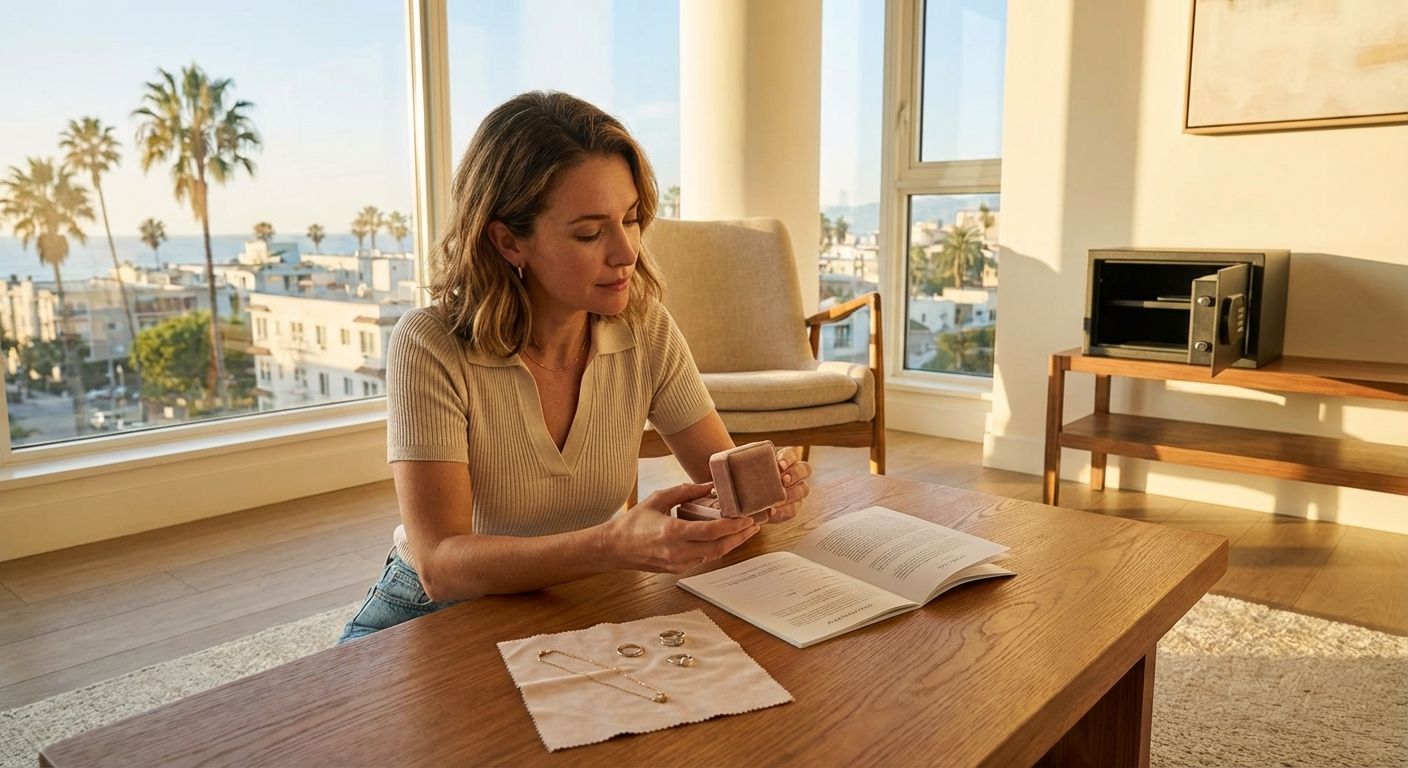

Scheduling Individual Items: The Gold Standard

This is the real answer for high-value jewelry. You can “schedule” specific items onto your renters insurance policy. Insurers often call this adding a “personal articles floater” or an “endorsement.” It’s like a mini-policy just for that one item.

To do this, you’ll need an appraisal from a certified jeweler. They’ll assess the item’s value, and then your insurance company — whether it’s State Farm, AAA, or Farmers — will cover it for that appraised amount. The beauty of scheduling? It usually covers many more perils than your basic policy, often including that tricky “mysterious disappearance.” Your ring could slip off your finger at the beach in Malibu, and you’d likely be covered. Big difference.

Understanding “All-Risk” vs. “Named Peril”

When you schedule an item, you’re often moving it from “named peril” coverage to “all-risk” coverage. “Named peril” means the insurance only pays if the loss is caused by one of the specific events listed in your policy. “All-risk,” on the other hand, means it covers *everything* unless a specific exclusion is listed. For jewelry, “all-risk” is what you want. It offers far broader protection.

The Appraisal Trap

An appraisal isn’t a one-and-done deal. Jewelry values can change. Gold and diamond prices fluctuate, and inflation happens. Most insurers want an updated appraisal every few years — maybe every three to five years. If you had your grandmother’s antique brooch appraised back in 2005, and it’s now 2024, that old appraisal might not reflect its true value today. If you have a claim, the insurer will only pay up to the *appraised value* on file. Make sure your appraisals are current.

What About Earthquake or Wildfire Damage to My Jewelry? California Specifics

Living in California means thinking about things like earthquakes and wildfires. It’s just part of the deal, whether you’re in San Francisco or the Inland Empire.

Earthquake damage to your jewelry? Not usually covered by your standard renters policy. Earthquake insurance is almost always a separate policy or an endorsement you have to add. If the ground shakes and your jewelry box tumbles, damaging those precious pieces, you’d need that specific earthquake coverage.

Wildfire, on the other hand, is usually considered a “fire” peril. So, if your apartment in, say, Ventura County, is impacted by a wildfire — and we’ve seen plenty of those — your standard renters policy would likely cover your jewelry loss up to your policy’s limits, including those sub-limits we talked about. But here’s the thing. If you live in a really high-risk fire area, some insurers might be hesitant to even offer a standard policy, or your premiums could be higher. It’s a challenging market for property insurance in California right now.

Is It Really Worth It? The Cost vs. Peace of Mind

Honestly, for the price of a few lattes a month, renters insurance itself is incredibly affordable, especially compared to homeowners insurance premiums which have jumped significantly in recent years. Adding a personal articles floater for your valuable jewelry is an additional cost, yes. But it’s often a surprisingly small amount compared to the value of the item it protects. We’re usually talking about an extra $10 to $20 a year for every thousand dollars of coverage.

Think about it. That $10,000 engagement ring could cost you an extra $100-$200 a year to fully protect, even against mysterious disappearance. Is that worth the peace of mind knowing you won’t be out ten grand if it vanishes? Most people would say absolutely. It’s a smart financial move.

Ready to see how affordable protecting your valuables can be? Get a free quote today: https://affordablerentersinsurancecalifornia.com/quote/

What If I Move? Does My Jewelry Coverage Move With Me?

Good question. Generally, your renters insurance policy covers your personal property anywhere in the world, up to certain limits. So if you’re traveling for work or vacation, your scheduled jewelry is still protected.

But wait — if you move to a new apartment across town, you’ll need to update your address with your insurer. If you move out of state, you’ll definitely need a whole new policy from an insurer licensed in that state. Renters insurance is state-specific.

A Word From a California Pro: Karl Susman’s Take

Navigating the ins and outs of renters insurance, especially when it comes to high-value items like jewelry, can feel like a maze. That’s why talking to an experienced agent is so important. Karl Susman, with Affordable Renters Insurance California, has been helping Californians understand their insurance needs for years. He’s seen firsthand how often people are underinsured for their most treasured possessions.

“Many folks just check the box for renters insurance, thinking they’re covered,” says Karl Susman. “But they don’t realize the specific limits on jewelry until it’s too late. An appraisal and a personal articles floater are key for true protection. It’s about being proactive, not reactive.”

Don’t leave your precious jewelry vulnerable. Reach out to Karl Susman at Affordable Renters Insurance California, CA License #OB75129, by calling (877) 411-5200. Or, if you’re ready to explore options for your renters insurance and jewelry coverage, get a quote here: https://affordablerentersinsurancecalifornia.com/quote/

Frequently Asked Questions About Jewelry & Renters Insurance

Does a safe deposit box protect my jewelry from everything?

A safe deposit box is great for preventing theft or damage from a fire or flood in your home. It’s a smart move for items you don’t wear often. However, it won’t protect against “mysterious disappearance” if you lose the item *before* putting it in the box or *after* taking it out. And if the item is damaged *while* you’re wearing it, the box won’t help. It’s a security measure, not an insurance policy.

What if I bought my jewelry out of state? Does that affect coverage?

Not at all. Where you bought the jewelry makes no difference to your California renters insurance policy. What matters is where you live, where the policy is issued, and whether the item is properly appraised and scheduled.

Can I get jewelry coverage without renters insurance?

Yes, you can. It’s called a standalone personal articles policy. Some people opt for this if they have incredibly valuable jewelry but don’t need or want a full renters policy. However, it’s often more cost-effective to add a floater to an existing renters insurance policy, as the base policy spreads out some of the administrative costs.

Is costume jewelry covered by renters insurance?

Yes, costume jewelry is covered, just like any other personal property. However, it will only be covered up to its actual cash value, which for most costume pieces is very little. It’s also still subject to your policy’s overall personal property limits and any specific jewelry sub-limits. Don’t expect a big payout for your fun, inexpensive pieces.

What’s the difference between replacement cost and actual cash value for jewelry?

This is a big one. “Actual cash value” (ACV) takes depreciation into account. If your ten-year-old watch is stolen, ACV would pay you what that watch is worth *today*, factoring in its age and wear. “Replacement cost,” on the other hand, pays you what it would cost to buy a brand-new, similar watch. For jewelry, especially scheduled pieces, you almost always want replacement cost coverage. It ensures you can truly replace what you lost without being out of pocket for depreciation.

This article is for informational purposes only and does not constitute financial advice.